Ethics in the Digital Age: Challenges for Modern Accountants

The profession – Accountant is evolving rapidly due to digital transformation, automation, artificial intelligence, and big data. While technology improves efficiency and strengthens compliance, it also introduces new ethical challenges. Modern accountants must navigate these challenges with strong professional ethics, just as emphasized by the ACCA Ethics and Professional Skills Module (EPSM). Understanding ethical responsibilities in today’s digital age is essential for future accountants who want to build trustworthy, credible careers.

Digital Transformation and the Ethical Landscape

Digital tools now play a major role in accounting functions — from cloud-based accounting systems to data analytics dashboards and AI-assisted audits. The ACCA highlights that technology amplifies the importance of transparency, confidentiality, and public trust. As data becomes more accessible, accountants must ensure decisions remain consistent with ethical principles such as integrity, objectivity, professional competence, due care, and confidentiality.

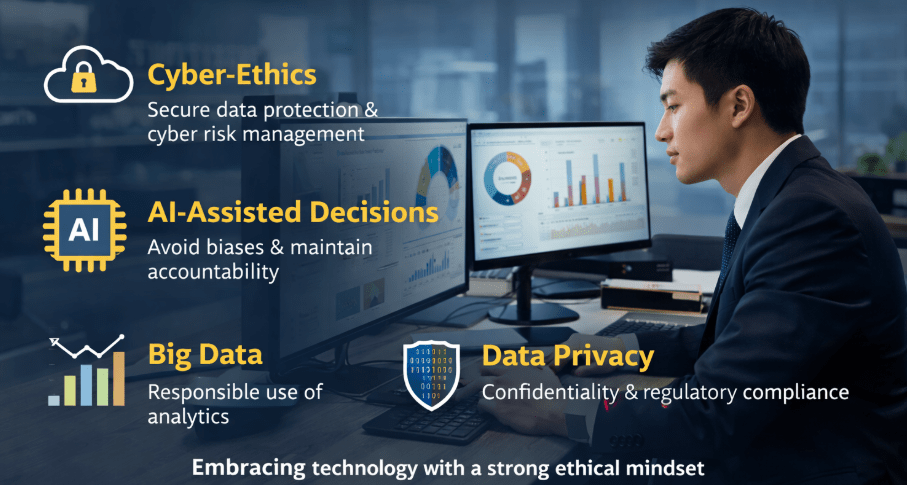

Cyber-Ethics and Data Protection

Cybersecurity has become one of the most pressing ethical concerns in accounting. Financial data is highly sensitive and often targeted by hackers. Data breaches not only cause financial loss but also damage organisational credibility and trust.

Accountants working with digital systems must understand:

-

Data confidentiality obligations

-

Secure storage and transmission of financial information

-

Regulatory requirements (e.g., PDPA, GDPR)

-

Cyber risk management frameworks

The ACCA stresses that professional accountants act as guardians of financial data. Ethical responsibility extends beyond compliance — it involves protecting stakeholders from digital threats and promoting secure digital practices within organisations.

AI-Assisted Decision-Making: Ethical Questions

Artificial intelligence is transforming audit, tax, and reporting processes. AI tools can detect anomalies, assess risk, and automate repetitive tasks. While AI enhances efficiency, it raises ethical concerns related to:

-

Bias in algorithms

-

Lack of transparency in automated decisions

-

Overreliance on machine outputs

-

Accountability in cases of error

ACCA guidance reminds students that professional skepticism is still essential — even when technology is involved. Accountants must evaluate AI-generated results critically instead of accepting outputs blindly. Human judgment remains central to ethical decision-making.

Another concern is accountability. If AI tools misinterpret financial data or produce flawed audit insights, the responsibility still lies with the professional accountant. Ethical standards ensure that technology supports judgment but never replaces it.

Big Data, Analytics, and Ethical Use of Information

Modern accountants use big data to support forecasting, financial modelling, and business insights. However, ethical challenges arise regarding:

-

Data ownership

-

Data privacy

-

Informed consent

-

Misuse of analytics for manipulation or discrimination

The ACCA notes that ethical analysis must accompany technical analysis. Just because data can be collected does not mean it should be. Students must learn to balance analytical capability with ethical restraint.

Social Responsibility and Public Interest

A core component of accounting ethics is serving the public interest. The digital economy introduces new stakeholders: consumers, regulators, platforms, and data subjects. Ethical accounting decisions may involve considerations such as:

-

sustainable reporting,

-

ESG (Environmental, Social & Governance) disclosures,

-

and responsible use of technology.

Digital transformation brings faster reporting and broader transparency expectations. Modern accountants are increasingly expected to promote accountability not only within organisations but also across society.

Ethical Mindset for the Future Accountant

The ACCA EPSM emphasizes the importance of developing an ethical mindset, not just technical competence. In the digital age, this mindset includes:

✔ Awareness of digital risks

✔ Critical evaluation of AI systems

✔ Data governance and privacy knowledge

✔ Professional skepticism toward automated outputs

✔ Commitment to public trust and social responsibility

Future accountants must cultivate soft skills such as judgment, communication, and ethical reasoning. These skills complement digital tools and ensure technology supports — instead of replacing — professional values.

Final Thoughts

Technology is reshaping the accounting profession, but ethical principles remain as important as ever. Students exploring accounting studies should recognize that the future accountant is not only a technical expert but also a responsible digital professional. As ACCA emphasizes, strong ethical foundations ensure that digital transformation leads to better decisions, stronger organisations, and greater public trust. Ethical behavior will continue to define excellence in accounting, no matter how advanced technology becomes.

Read More:

Accounting ethics in the digital age: https://www.accaglobal.com/my/en/student/exam-support-resources/professional-exams-study-resources/strategic-business-reporting/technical-articles/ethics-digital.html

ACCA Ethics and Professional Skills Module (EPSM): https://blog.fame.edu.my/10-units-in-acca-epsm/